Fed Signals Three Cuts; Gold Keeps Its Shine

Although the results of the meeting of the Federal Reserve (‘the Fed’) on 20 March weren’t very surprising and generally in line with December’s quarterly forecast, gold moved up to a fresh all-time high while the dollar declined. Participants in major markets seem to be positive due to the stability of the Fed’s projections; sentiment on gold in particular is strong. This article summarises recent events leading to the Fed’s latest hold and looks briefly at the charts of XAUUSD and EURUSD.

Projections of nine total cuts by the end of 2026 would take the funds rate to 3-3.25%, still moderately restrictive. That scenario would be very likely to prevent a significant resurgence of inflation unless there were strong external influences, such as the price of oil. A fairly large majority of participants now expects a cut in June, around 68% according to CME FedWatch Tool.

Overall, the USA seems to be doing the best among major, advanced economies. ‘Necessary economic slowdown’ has been dropped; there’s no indication from GDP data that the Fed needs to cut more rapidly to avoid a recession:

Although the second estimate of the fourth quarter’s GDP at 3.2% was negligibly lower than the advance, it remains much stronger than any other large economy. The Fed revised estimates for the next three years upward at its latest meeting. Sustaining this level of growth despite restrictive monetary policy shows the resilience of the American economy and reduces the pressure on the Fed to loosen quickly now that inflation has stabilised:

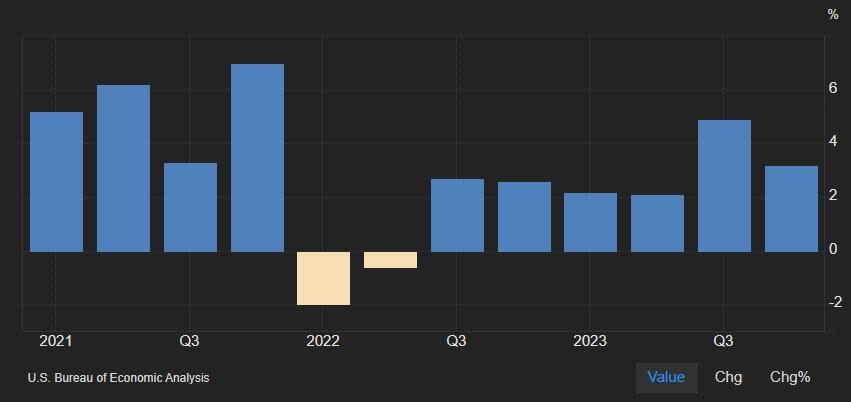

Headline inflation has been consistently higher than the consensus since late 2023, which seems likely to continue, but in most cases there hasn’t been a large surprise. The rate has generally settled around 3-4% but has some way to go before reaching 2% consistently. As noted above, general economic conditions aren’t putting strong pressure on the Fed to get the job done as soon as possible; so far, a patient approach is working. This has some support from job data too:

The gradual slowdown in the job market since this time last year is one factor the Fed has been looking for to support intentions to loosen monetary policy. Growth in average earnings has also slowed down somewhat since 2022, but this hasn’t been a very consistent trend. A sudden spike in unemployment seems very unlikely now given the strength of GDP data.

It’s probably too early to start looking very closely at polling for the upcoming presidential election in November, so for the moment sentiment remains key for gold. In the absence of significant new information or narratives from economic data and monetary policy, gold might be expected to continue upward and the dollar down, but the latter depends also on how other major central banks act this summer. The European Central Bank might also start cutting in June, but the Bank of England is more likely to commence in August, while the Bank of Japan only just called for its first hike for 14 years earlier this week.