Analysts Have Been Trimming Their Transocean Ltd. (NYSE:RIG) Price Target After Its Latest Report

Transocean Ltd. (NYSE:RIG) shareholders are probably feeling a little disappointed, since its shares fell 6.0% to US$4.86 in the week after its latest yearly results. It was a moderately negative result overall - revenue fell 2.6% short of analyst estimates at US$2.8b, although at least statutory losses were marginally smaller than expected, at US$1.24 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

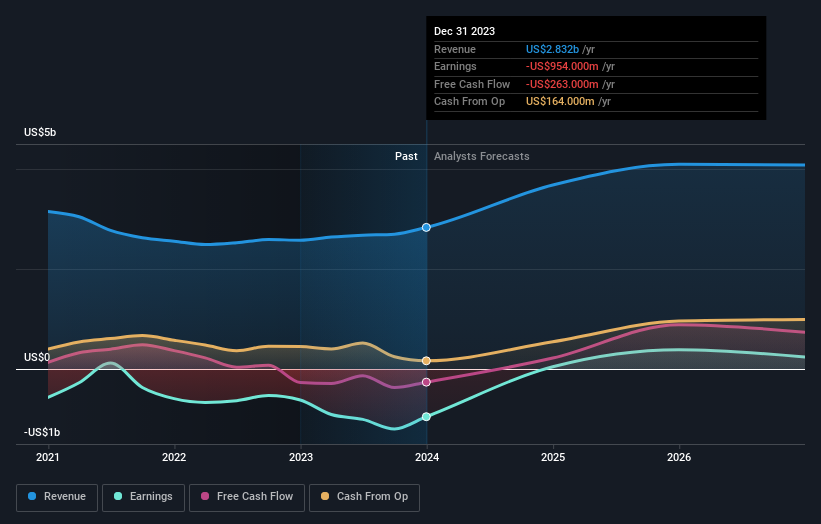

See our latest analysis for Transocean

Taking into account the latest results, the current consensus from Transocean's 13 analysts is for revenues of US$3.68b in 2024. This would reflect a huge 30% increase on its revenue over the past 12 months. Earnings are expected to improve, with Transocean forecast to report a statutory profit of US$0.036 per share. In the lead-up to this report, the analysts had been modelling revenues of US$3.77b and earnings per share (EPS) of US$0.17 in 2024. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a large cut to earnings per share numbers.

The consensus price target fell 9.0% to US$7.41, with the weaker earnings outlook clearly leading valuation estimates. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Transocean at US$12.00 per share, while the most bearish prices it at US$5.00. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Transocean's past performance and to peers in the same industry. One thing stands out from these estimates, which is that Transocean is forecast to grow faster in the future than it has in the past, with revenues expected to display 30% annualised growth until the end of 2024. If achieved, this would be a much better result than the 4.4% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 7.6% annually. Not only are Transocean's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.