Mettler-Toledo International, Inc. MTD reported fourth-quarter 2023 adjusted earnings of $9.40 per share, which missed the Zacks Consensus Estimate by 8.9%. The bottom line decreased 22% on a year-over-year basis.

Net sales of $934.99 million lagged the Zacks Consensus Estimate of $979.31 million. The figure declined 12% on a reported basis and 13% on a currency-neutral basis from the year-ago quarter’s respective readings.

Shipping delays of approximately $58 million from a new external European logistics provider was a major headwind for the company.

Weak momentum across the Industrial and Laboratory segments was a concern. Also, softness in Americas, Europe and especially in Asia/Rest of the World regions was negative.

MTD lost 19.1% in the past year, underperforming the industry’s decline of 13.4%.

Nevertheless, strong momentum in the Food Retail segment was a tailwind.

We believe the solid execution of the company’s Spinnaker and SternDrive programs is likely to aid its financial performance in the days ahead. Also, its portfolio strength, cost-cutting efforts, margin and productivity initiatives, as well as robust sales and marketing strategies, are expected to remain tailwinds.

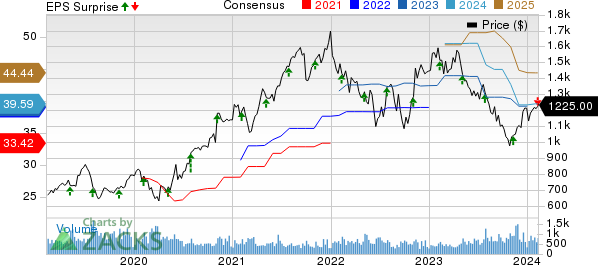

Mettler-Toledo International, Inc. Price, Consensus and EPS Surprise

Mettler-Toledo International, Inc. Price, Consensus and EPS Surprise

Mettler-Toledo International, Inc. price-consensus-eps-surprise-chart | Mettler-Toledo International, Inc. Quote

Top Line in Detail

By Segments: MTD reports revenues under three segments, namely Laboratory Instruments, Industrial Instruments and Food Retail, which accounted for 55%, 40% and 5%, respectively, of net sales in the fourth quarter. The Industrial and Laboratory segments witnessed a year-over-year decline of 7% and 18%, respectively, in the fourth quarter.

Nevertheless, the Food Retail segment witnessed growth of 9% year over year.

By Geography: Total sales from the Americas, Europe and Asia/Rest of the World contributed 43%, 28% and 29%, respectively, to net sales in the fourth quarter. Sales in the Americas, Europe and Asia/Rest of the World went down 7%, 16%, and 18%, respectively, on a year-over-year basis.

Operating Results

The gross margin was 59.0%, contracting 80 basis points (bps) year over year.

Research & development (“R&D”) expenses were $46.44 million, up 1% from the year-ago quarter’s figure. Selling, general & administrative (“SG&A”) expenses decreased 2% year over year to $223.43 million.

As a percentage of sales, R&D expenses expanded 70 bps year over year to 5%. SG&A expenses expanded 240 bps year over year to 23.9%.

The adjusted operating margin was 30.1%, which contracted 380 bps from the prior-year quarter’s level.

Balance Sheet & Cash Flow

As of Dec 31, 2023, Mettler-Toledo’s cash and cash equivalent balance was $69.8 million, up from $69.7 million as of Sep 30, 2023.

Long-term debt was $1.89 billion at the end of the fourth quarter, down from $1.93 billion at the end of the third quarter.

Mettler-Toledo generated $281.5 million in cash from operating activities in the reported quarter compared with $264.3 million in the previous quarter. Free cash flow was $260.13 million in the reported quarter.

Guidance

For first-quarter 2024, Mettler-Toledo anticipates sales to decline 4-6% in local currency from the year-ago quarter’s reported figure. The Zacks Consensus Estimate for first-quarter sales is pegged at $865.1 million.

Adjusted first-quarter earnings are anticipated to be $7.35-$7.75 per share, implying an 11-15% fall from the year-ago quarter’s reported number, which includes a foreign-currency headwind of 4%. The Zacks Consensus Estimate for earnings is pinned at $7.84 per share.

For 2024, Mettler-Toledo anticipates sales in local currency to be up 1-2% from the year-earlier figure. The Zacks Consensus Estimate for 2024 sales is pegged at $3.80 billion.

The company increased its guidance for adjusted EPS from $39.10-$39.80 to $39.60-$40.30. The new guided range suggests growth of 4-6% from the year-ago reported number, which includes a foreign-currency headwind of 2%. The Zacks Consensus Estimate for the same is pinned at $39.59.

Zacks Rank & Stocks to Consider

Mettler-Toledo currently has a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader technology sector are BlackLine BL, Arista Networks ANET, and Badger Meter BMI. While BlackLine and Arista Networks sport a Zacks Rank #1 (Strong Buy) each, Badger Meter carries a Zacks Rank #2 (Buy), at present.

You can see the complete list of today’s Zacks #1 Rank stocks here.

BlackLine shares have lost 1.1% in the year-to-date period. The long-term earnings growth rate for BL is currently projected at 50.56%.

Arista Networks shares have gained 17.1% in the year-to-date period. The long-term earnings growth rate for ANET is currently projected at 20.15%.

Badger Meter shares have lost 5.1% in the year-to-date period. The long-term earnings growth rate for BMI is currently projected at 12.27%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report