PepsiCo, Inc. PEP has reported robust fourth-quarter 2023 results, wherein earnings surpassed the Zacks Consensus Estimate and improved year over year. The top line missed the consensus estimate and declined year over year.

The results reflect gains from strength and resilience in its categories, diversified portfolio, modernized supply chain, improved digital capabilities, flexible go-to-market distribution systems, and robust consumer demand trends. However, soft volumes hurt the top line.

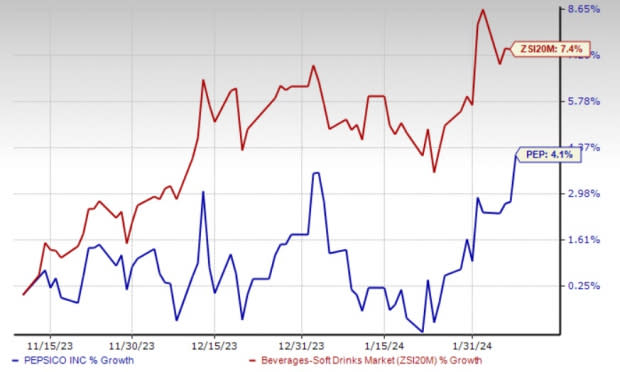

PEP shares declined 2.1% in the pre-market session following the earnings release on Feb 9, owing to soft fourth-quarter sales results. Shares of the Zacks Rank #3 (Hold) company have gained 4.1% in the past three months compared with the industry’s 7.4% growth.

Zacks Investment Research

Image Source: Zacks Investment Research

Quarter in Detail

PepsiCo’s fourth-quarter core EPS of $1.78 beat the Zacks Consensus Estimate of $1.72 and increased 6.6% year over year. In constant currency, core earnings improved 9% from the year-ago period, backed by the mitigation of inflationary pressures through cost-management and revenue-management initiatives. The company’s reported EPS of 94 cents rose 152% year over year in the quarter. Adverse currency rates impacted EPS by 2% in the quarter.

Net revenues of $27,850 million declined 0.5% year over year and missed the Zacks Consensus Estimate of $28,242 million. Revenues were impacted by a unit volume decline of 3% for the convenient food business and were down 2% for the beverage business. This was partly offset by an improved price/mix in the reported quarter. Foreign currency impacted revenues by 1.5%.

On an organic basis, revenues grew 4.5% year over year, driven by growth across categories and geographies. The consolidated organic volume was down 4%, while effective net pricing improved 9% in the fourth quarter. Pricing gains were driven by strong realized prices across all segments.

Our model predicted organic revenue growth of 6.2% for the fourth quarter, with a 9.6% gain from price/mix and a 3.5% decline in volume.

PepsiCo, Inc. Price, Consensus and EPS Surprise

PepsiCo, Inc. Price, Consensus and EPS Surprise

PepsiCo, Inc. price-consensus-eps-surprise-chart | PepsiCo, Inc. Quote

On a consolidated basis, the reported gross profit increased 1.2% year over year to $14,753 million. The core gross profit rose 1.3% year over year to $14,898 million. The reported gross margin expanded 91 basis points (bps), whereas the core gross margin expanded 97 bps.

We anticipated the core gross margin to expand 30 bps to 52.8%. In dollar terms, core gross profit was expected to increase 1.4% year over year.

The reported operating income of $1,683 million rose 106% year over year. The core operating income grew 8.7% year over year to $3,185 million and the core constant-currency operating income improved 10%. The reported operating margin expanded 313 bps from the year-ago quarter. Meanwhile, the core operating margin expanded 97 bps due to ongoing holistic cost-management initiatives to drive superior supply chain and distribution efficiencies.

Our model predicted core SG&A expenses of $11.9 billion, which indicated year-over-year growth of 1.1%. As a percentage of sales, core SG&A expenses were anticipated at 42.1%, flat with the prior-year quarter.

We expected a core operating margin of 10.6%, with a 10-bps expansion from the year-ago quarter’s actual.

Segmental Details

The company witnessed revenue declines across most segments. Organic revenues improved for all segments, except for QFNA and APAC.

Revenues, on a reported basis, declined 3% year over year in FLNA, 16% in QFNA, 2% in PBNA, 1% in Europe, 4% in AMESA, and 2% in APAC. However, revenues improved 18% in Latin America in the fourth quarter. Organic revenues increased 3% for FLNA, 3% for PBNA, 8% for Latin America, 10% for Europe, and 11% for AMESA. Organic revenues declined 10% for QFNA and 1% for APAC.

Financials

The company ended 2023 with cash and cash equivalents of $9,711 million, long-term debt of $35,595 million, and shareholders’ equity (excluding non-controlling interest) of $18,503 million.

Net cash provided by operating activities was $13,442 million as of Dec 30, 2023, compared with $10,811 million as of Dec 31, 2022.

Outlook

PepsiCo outlined its view for 2024. The company expects organic revenue growth of at least 4% for 2024. It anticipates core constant-currency EPS growth of at least 8% from the year-ago period’s reported figure.

PEP expects currency headwinds to hurt revenues and core EPS by 1 percentage point in 2024, based on the current rates. The company expects a core effective tax rate of 20% for 2024.

Based on the above assumption, PepsiCo expects a core EPS of at least $8.15 for 2024. This suggests a 7% increase from the core EPS of $7.62 reported in 2023.

PepsiCo has been committed to rewarding shareholders through dividends and share buybacks. It expects to return a value worth $8.2 billion in 2024, including $7.2 billion of dividends. Additionally, the company plans to repurchase shares worth $1.0 billion in 2024.

Don’t Miss These Better-Ranked Stocks

We have highlighted three better-ranked stocks from the Consumer Staple sector, namely Coca-Cola FEMSA KOF, The Boston Beer Company SAM and Molson Coors TAP.

Coca-Cola FEMSA currently flaunts a Zacks Rank #1 (Strong Buy). KOF shares have rallied 18.5% in the past three months. You can see the complete list of today's Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Coca-Cola FEMSA’s current financial-year sales and EPS suggests growth of 25.8% and 28.2%, respectively, from the year-ago period’s reported figures. KOF has a trailing four-quarter earnings surprise of 16.5%, on average.

Boston Beer currently sports a Zacks Rank #1. SAM shares have risen 4.5% in the past three months. The company has a trailing four-quarter negative earnings surprise of 77.7%, on average.

The Zacks Consensus Estimate for Boston Beer’s current financial-year sales suggests a decline of 4.1% from the year-ago period’s reported figure. The consensus mark for the company’s earnings per share indicates growth of 2.7% from the year-ago quarter’s reported number.

Molson Coors has a trailing four-quarter earnings surprise of 41.3%, on average. It currently carries a Zacks Rank #2 (Buy). TAP shares have gained 2.2% in the past three months.

The Zacks Consensus Estimate for Molson Coors’ current financial-year sales and earnings suggests growth of 9.2% and 30.7%, respectively, from the year-ago period's reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report